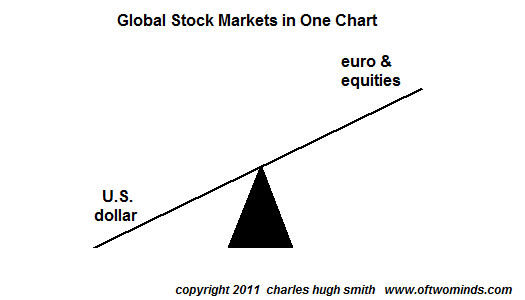

If we dispense with all the fancy stuff, we end up with a simple see-saw with the euro and global equities on one end and the much-hated U.S. dollar on the other.

If we scrape away the ever-hopeful headlines predicting a new figurehead lackey or another vote will magically fix Greece, Italy, the euro, Europe's crumbling banks, etc., the global stock markets can be distilled down to one chart. And here it is: a see-saw with the U.S. dollar on one end and the euro and equities on the other.

I know the mind rebels at such simplicity, and so does the entire buy-side Wall Street edifice: if it all boils down to this, then there really isn't much value added by the endless reams of fancy reports and analysis, is there?

But let's presume for a moment that it really is this simple. Where does that leave global stock markets? The answer can be had by glancing at two other charts: one of the euro and one of the dollar.

Now that the cargo-cult chiefs are openly talking about the euro splintering into euro 1 and euro 2 (i.e. business class and steerage), something I proposed as a possible "face-saving" step in the devolution of the euro 18 months ago ( Why the Euro Might Devolve into Euro 1 and Euro 2 March 2, 2010), then the common-sense question is: why is the euro worth 36% more than the dollar? The answer is that it isn't worth 36% more, of course, and for a bit of technical support of that we turn to a simple chart.

There's not much to support Bulls' claims of euro strength here and much to suggest the euro is in a leaky barrel floating helplessly toward Niagara Falls. Classic wedge broken decisively to the downside, check. Uptrend decisively broken, check. RSI declining but not oversold, check. MACD declining and below the neutral line, check. Price below the critical 200-week moving average (MA), check. Price below the equally critical 50-week MA, check.

The last time these conditions occurred (April 2010), the euro cliff-dived from right where it is now around 136 to 120 in a few weeks. Technically, there are numerous reasons to consider this a high-probability scenario and essentially no support for the notion that the euro is about to storm higher.

And as the euro goes, so go equities.

Meanwhile, the chart of the dollar is unsurprisingly the inverse of the euro: it's loaded with bullish bits. RSI rising, check. MACD rising and above the neutral line, check. Classic wedge broken to the upside, check. Downtrend decisively broken, check. Classic A-B-C-D pattern visible, check. Price above the critical 50-week moving average, check.

In another classic move, price kissed the 200-week MA, retraced to support, and is now rising back to break through the resistance offered by the 200-week MA.

Without getting too fancy, the obvious targets for the euro are 120 and parity with the dollar at 100. This could also be seen as reversion to the mean. The targets for the DXY (dollar index) are correspondingly 88-90 and 100-105.

As for what this means for equities, it's a free-for-all limbo dance: how low can you go? The S&P 500, currently around 1,240, could easily limbo down to the psychological 1,000 level, pause to towel off the sweat and then repeat its 2008 swan dive to 666. Or maybe not. The only thing the see-saw tells us for certain is the euro and equities are on one end and the dollar is on the other. If the euro tanks, equities tank, too.

I know, I know, the dollar is doomed, it can't possibly rise, blah blah blah. If you insist on a fundamental reason, then read this: banks are short currency, long assets (Zero Hedge).

And what's holding up the euro again? I'm getting a lot of static in the answer.

No comments:

Post a Comment