The Bank of Canada has been fretting about the ballooning debt of

Canadian households. Last year, it repeatedly called it a risk to

“financial stability,” perhaps in preparation for raising its benchmark

interest rate. Then Canada’s economy tanked.

In July, when the freaked-out Bank of Canada cut its benchmark rate

for the second time this year,

it admitted that the rate cut comes at the price of “financial

stability risks” which “remain elevated.” Governor Stephen Poloz added:

“Of particular note are the vulnerabilities associated with household

debt and rising housing prices.”

These rate cuts didn’t do much to support Canada’s resource economy

that has been spiraling down in the wake of the commodities rout. But

they made up for it by inflating the housing bubble even further.

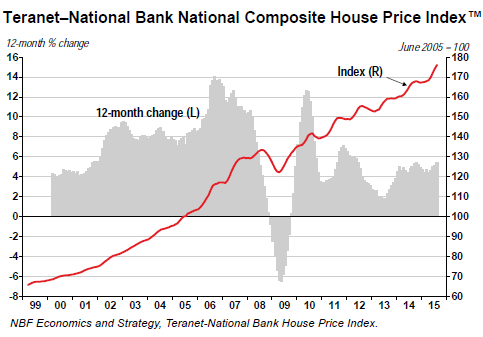

The Teranet–National Bank house price index, released September 14,

hit new records every month this year. In August, it was up 5.4%

year-over-year. Note how the index has soared since the peak of the

prior housing bubble that ended with the Financial Crisis:

The index masks what Marc Pinsonneault, senior economist at NBF’s

Economics and Strategy,

calls the “dichotomy” of Canada’s housing market. In some cities, price

increases are cooling, year over year: Victoria +3.2%, Edmonton +0.8%,

Calgary +0.7%. In other cities, prices are actually falling

year-over-year: Winnipeg -0.4%, Ottawa-Gatineau -0.4%, Montreal -0,5%,

Quebec City -0.7%, and Halifax -1.4%.

But they’re sizzling in Vancouver +9.7%, Hamilton +8.8%, and Toronto +8.7%. And prices for

non-condo homes in Vancouver and Toronto – the two cities account for 54.1% of the index – jumped over 10%!

On cue, total

consumer debt

rose 4.9% year-over-year in July to C$1.86 trillion. A trend that has

been picking up speed recently: on a monthly basis, consumer debt jumped

in July at an annualized rate of 5.4%. Mortgage debt – over two-thirds

of total consumer debt – soared at an annualized rate of 6.9%.

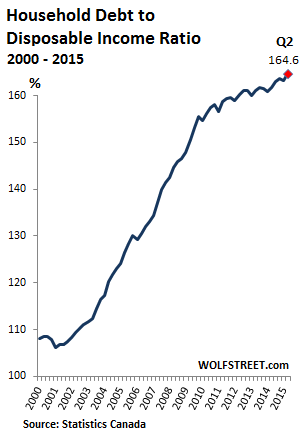

Yet disposable incomes only inched up 0.8% in the second quarter,

Statistics Canada

reported on September 11. So the household-debt-to-disposable-income

ratio, a measure of household leverage, hit a record 164.6%, the largest

jump in the ratio since 2011:

“Fortunately, there’s little need to fret about households’ ability

to carry all that debt,” BMO Capital Markets senior economist Benjamin

Reitzes wrote in a

note.

Interest rates are super-low, and thus the burden of carrying all this

debt still manageable. But even he conceded that “further increases

would start to ramp up our level of concern.”

The ratio is an average. There are many Canadian households with

little or no debt. But then there are many other households whose

incomes have not fared well, and who have piled on debt to buy a modest

home in one of the most overpriced housing markets in the world.

And they’re not just borrowing to buy homes. In its consumer credit report for the second quarter, released September 15,

Equifax Canada

reported that auto-loan balances increased by 3.9% year-over-year. And

installment-loan balances (credit cards, etc.) jumped 8.0%.

Consumers are beginning to stretch.

But no problem. Despite increased debt loads, the 90-day-plus

delinquency rate is down 1.6% and bankruptcies are down 9.4%, Equifax

reported, as they should be, given the increasingly easy and cheap

credit sloshing through the land: borrowers aren’t going to fall behind

if they keep getting new money. It’s when they can’t get anymore new

money….

But suddenly there are problems: rising delinquencies in “some of the sub-segments” of the population, the report warned.

We’re starting to see the impact of low oil prices in the

West as these prices are forcing a new reality on Alberta and

Saskatchewan in particular. In these two provinces the debt levels are

stable, but the delinquency rate has started to increase.

On a demographic basis, the 90+ day delinquency rate for Canadians

aged 65+ rose for the first time since 2010. The rate increased by 2.4%

this quarter versus a decrease of 5.1% in the previous quarter.

So the oil patch is experiencing rising delinquencies. And across

Canada, for the first time since the Financial Crisis: seniors!

Equifax promised to “monitor this trend closely in the coming quarters.”

This ballooning household debt “puts Canadian consumers in a

precarious situation,” Scott Hannah, CEO of the non-profit Credit

Counselling Society, told the

Toronto Star.

“If they’re struggling to manage their increasing debt obligations now,

a sudden change in external factors — like a rise in interest rates or

the loss of a job — will leave many Canadians in greater financial

difficulty.”

It’s for a reason that the Bank of Canada called this enormous amount

of household debt a “financial stability risk.” The fact that

delinquencies have started to rise in the first subsectors – despite

historically low interest rates and super-easy money – is the audible

ticking of a time bomb under one of the most overpriced housing markets

in the world.

Spiking numbers of “half-empty” office buildings? “Canada is also in

the midst of an ill-timed supply surge that caused vacancy rates to

rise, warns a new report. It paints a picture of an epic office boom

turned into an epic office glut.