In his famous book A Random Walk Down Wall Street, Burton Malkiel suggests that every stock is exactly fairly valued. There can be no such thing as an undervalued stock or an overvalued stock, since investors are armed with all knowledge impacting the value of a stock. With all due respect to the Princeton professor, he's wrong. Very wrong. Stock valuations are a function of supply and demand, and right now, demand for stocks is weak and stock prices have fallen far below their intrinsic value.

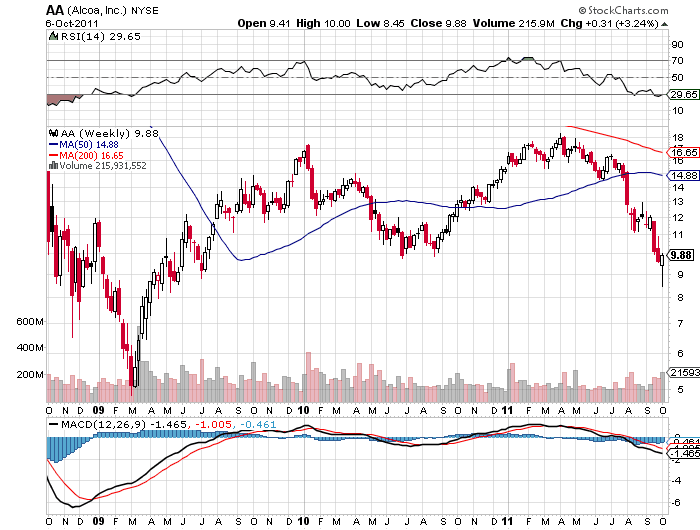

In his famous book A Random Walk Down Wall Street, Burton Malkiel suggests that every stock is exactly fairly valued. There can be no such thing as an undervalued stock or an overvalued stock, since investors are armed with all knowledge impacting the value of a stock. With all due respect to the Princeton professor, he's wrong. Very wrong. Stock valuations are a function of supply and demand, and right now, demand for stocks is weak and stock prices have fallen far below their intrinsic value. I was reminded of this once again as I was poring over the financial statements of Alcoa (NYSE: AA) as the aluminum giant gets set to kick off earnings season next week. The company's stock touched a two-year low on Tuesday, Oct. 5, and now trades at levels seen back in 1995. Make no mistake, Alcoa is a very healthy company poised for robust cash flow, regardless of what the stock price may tell you.

Why the sell-off?

Investors are surely concerned about the global economy and what that might mean for pricing and demand for Alcoa's three main businesses: alumina, aluminum and finished aluminum products.

Falling aluminum spot prices

The recent drop in the stock off should tell you two things. First, the consensus EPS (earnings per share) forecast of $0.27 simply won't happen. Analysts had been basing their profit forecasts on aluminum in the $1.10 to $1.15 range. If I had to make a guess, Alcoa will earn closer to $0.15 a share. (That's not to say shares will take a hit when the numbers come out -- the recent stock selloff already anticipates a shortfall, in my opinion.)

The other thing to infer from the recent selloff: this stock is now absurdly cheap by so many measures and can pay off big for those with a multi-year timeline.

2009 Redux?

Investors may be bracing for a return to the brutal industry conditions of 2009, when aluminum prices skidded to around $0.65 per pound, leading Alcoa to lose $1.05 a share for the full year. Since then, several factors have changed, and although Alcoa's pricing and profits may indeed slump further in coming weeks and months, they shouldn't hit 2009 levels. And when demand rebounds, Alcoa's financial performance should be outstanding. Remember: you should buy a stock when an eventual bottom is in sight, not when the bottom has already passed.

The China factor

Alcoa's financial results peaked in 2007, when the company generated 21% EBITDA margins and earned $3.24 a share. The robust results masked the fact that China was wreaking havoc with the aluminum industry by producing more than it consumed. Not anymore. For the first time since 2002 (with the exception of 2009), China now consumes more aluminum than it produces, which means Alcoa faces less pressure in terms of Chinese aluminum imports. It can now count on China as an export market.

Why the change? Because policy planners in China have belatedly realized that it's more economical to rely on aluminum imports because Chinese smelters consume far more energy than those operated by Alcoa and others. High-cost Chinese smelters are being shuttered, and the country's total output is expected to shrink in 2012 and again in 2013.

Alcoa has made a series of investments during the past five years to open smelters where power costs are very low, such as Iceland (hydro-electric), Trinidad (natural gas) and Saudi Arabia (natural gas). The company's low-cost production base is finally turning into a competitive weapon. On the upcoming quarterly earnings conference call, listen for management's discussion of its own costs compared with the rest of the industry, and you'll see a bright picture emerging.

There's another reason to focus on the brightening long-term outlook for Alcoa. This is no longer just about soda cans. Aluminum is becoming a major component in airplanes, and more notably automobiles. In the next two years, a wide range of automakers will roll out vehicles with an increasing percentage of lightweight aluminum in their bodies. Audi and Jaguar started the trend, and others are now following suit. In response, Alcoa recently invested $300 million in a plant in Iowa that will produce more aluminum panels for automakers.

Running through the numbers

Clearly, Alcoa's shares are responding to near-term concerns. But as the market finds a bottom and investors go in search of value, they'll start to focus on just how cheap this stock is in relation to its long-term outlook.

For example:

- Alcoa sports $15 billion in book value, but is valued at just $9.4 billion on the market. Goldman Sachs sees book value per share rising to $17.91 by the end of 2013 -- twice the current stock price. Their target price is $16, up from a current $9.

- Citigroup anticipates Alcoa's operating cash flow will rise from $2.7 billion in 2010 to $3.7 billion by 2012.

- UBS, which sees shares rising to $13, notes shares are simply too cheap at 4.5 times projected 2013 EBITDA, on an enterprise value basis. They look for a big breakout in 2013, predicting net income will nearly double and free cash flow rises by half to $5.2 billion.

Risks to consider: China remains the wildcard. A major slowdown in its economy would keep aluminum prices depressed. As a silver lining, a period of low prices would shake out Alcoa's higher-cost rivals, helping the company to expand market share.

Action to Take --> This is a good company with an ugly stock. Shares have been in freefall for weeks now and have lost more than half their value in the past 52 weeks. Yet the long-term picture is inarguably bright for Alcoa. Investors may get a modest relief rally when quarterly results are released next week, and in the next few years, shares could well return to that 52-week high, at least double current levels.