Tuesday, August 30, 2011

Value Play: Arch Coal (ACI)

In the last 2 days, stocks have come back to claim almost half of the value that was lost

In the last 2 days, stocks have come back to claim almost half of the value that was lost in the August correction. However, there are still some stocks out there that took such a beat-down that they still present a valuable buying opportunity. One such stock is Arch Coal (ACI).

in the August correction. However, there are still some stocks out there that took such a beat-down that they still present a valuable buying opportunity. One such stock is Arch Coal (ACI).

After today's rally, shares are currently trading at $20.27 a share. Over the past 12 months, Arch Coal Inc (ACI) shares have traded between $16.91 and its 52-week high of $36.99. Arch Coal Inc shares are now trading with a P/E Ratio of 19.4 and EPS of 0.98.

Dahlman Rose & Co. analyst Daniel Scott wrote in a note to investors that the sector should see gradually increasing volumes for its products. He expects to see rising prices for thermal coal in the U.S., which is used to generate electricity. Prices for hot-burning metallurgical coal used to make steel will remain flat in 2013 after dropping from current high levels into 2012, Scott wrote:

Scott wrote that producers suffered from high costs, but he sees cost inflation moderating from current levels.

He released his 2013 earnings forecasts, ratings and 12-month price targets for U.S. coal producers:

-- Arch Coal Inc.: Reiterated "Buy" rating and price target of $38. Estimated earnings per share of $1.82 in 2011, $3.88 in 2012 and $4.29 in 2013.

Another Bear Market Coming? Here’s How To Avoid Its Bite

So says John Nyaradi (wallstreetsectorselector.com) in an article* which Lorimer Wilson, editor of www.munKNEE.com (It’s all about Money!), has further edited ([ ]), abridged (…) and reformatted below for the sake of clarity and brevity to ensure a fast and easy read. Please note that this paragraph must be included in any article re-posting to avoid copyright infringement. Nyaradi goes on to explain:

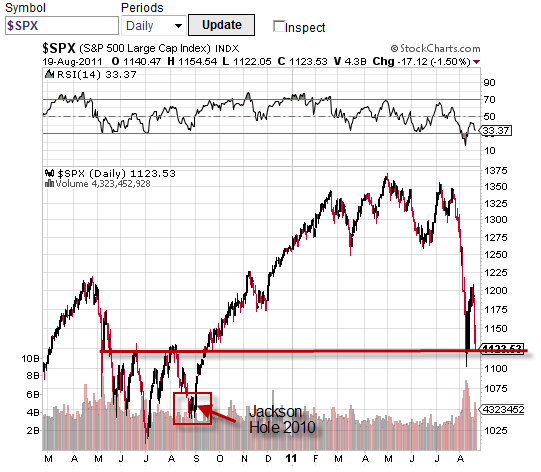

click to enlarge

Chart courtesy of stockcharts.com

In the chart of the S&P 500, above, you can see how the index has taken a sharp decline since the highs of mid-July. It is now below its 200 day and 50 day moving averages (red and blue lines) and has broken several long term trend lines. Furthermore, the 50 ma has crossed below the 200 day ma, forming what is widely known as the “death cross” which is a quite reliable statistically proven technical indicator [see here (1) for a recent article on the current "death cross" event]. While not perfect, as no indicator is, the “death cross” has managed to sidestep the biggest part of every recent bear market, while its counterpart, the “golden cross” has captured significant gains during bull markets.

However, it should also be noted that support at the 1120 level has been tested several times and so now the bears will have to push through that level to confirm that we are actually in the beginning days of a new bear market.

It is my opinion that this trading range will not continue for very long and that we’ll see a directional breakout, either up or down, within the next few weeks. Technical and fundamental conditions would indicate that the likely probability of that move would be down. If that turns out to be the case, as investors and traders, we have several choices if we believe a new bear market is upon us:

- to “buy and hold” which is the conventional wisdom and which I believe is quite ineffective in today’s volatile markets since the major indexes are still far below where they were in 2000 at the beginning of the “tech wreck” more than 11 years ago.

- to head for the safety of cash which many investors have done or to head for the safety of Treasury bonds and bills which have also seen a huge influx of funds in recent months and days. This strategy gets you out of harm’s way if the market indeed does continue its downward trajectory.

- to actually attempt to profit from declining markets and to do that, investors/traders today can use inverse exchange traded funds that move opposite to the action of the underlying index…

- to use put options, either as portfolio insurance on currently held positions or as directional bets in search of profits.

So from the above discussion we can conclude that we are at the very least in a significant correction of an ongoing bull market or either in or close to entering a new bear market. Coming days will tell us which way things will go and confirm this one way or other.

Conclusion

Whatever happens, exchange traded funds offer the power and flexibility to seek profits in any market environment.

Rice May Rally 22% by Yearend as Thai Buying Elevates Costs, Curbs Exports

Rice may rally 22 percent by yearend as Thailand, the world’s largest exporter, buys the grain from farmers at above-market rates, pushing up costs for importers and fanning global inflation even as economic growth slows.

The price of 100 percent grade-B Thai rice, the regional benchmark, may rally to $750 per metric ton by Dec. 31, according to the median estimate in a Bloomberg News survey of seven exporters, traders and millers conducted last week. That target is $50 higher than the median estimate in a separate Bloomberg survey undertaken in the first half of this month.

The surge may complicate matters for central bankers and policy makers around Asia who are already struggling to cool rising prices. Rice was the only grain separating the world from a food crisis, Abdolreza Abbassian, senior economist at the United Nations Food & Agriculture Organization, or FAO, said in February when worldwide food costs rallied to a record.

“If the sources of supply are actually inflating the prices for their commodities, regardless whether there’s supply or not, that’s going to keep prices elevated,” Abah Ofon, an analyst at Standard Chartered Plc, said by phone from Singapore. “That would keep risks for food inflation elevated.” (more)

Is the S&P500 Cheap?

I was somewhat surprised by a Bloomberg article discussing how cheap the S&P is (mentioned here this AM). Its not that Bloomie has suddenly become a cheerleader, but rather, this piece reflects the beliefs of a large chunk of classically trained value mutual fund managers.

Here’s a Bloomberg excerpt:

“At 1,176.80, the S&P 500 is trading at 10.8 times analysts’ forecast for profits in the next 12 months of $109.12 a share. For the P/E ratio to reach its five-decade average of 16.4 without shares appreciating, earnings would have to fall to about $71.76 a share, 22 percent below the last 12 months, data compiled by Bloomberg show.

Should companies meet analysts’ profit estimates, the S&P 500 must advance to about 1,790 to trade at the average multiple of 16.4 since 1954, according to data compiled by Bloomberg. That’s more than 50 percent above its last close. Futures on the S&P 500 expiring next month gained 1 percent to 1,185.9 at 7:48 a.m. in London today.” (emphasis added)

Of course, left unsaid is what if analysts estimates are too high; Historically, the fundie community has overestimated earnings growth by a factor of 2X.

Also unsaid was the impact of recession on earnings. A 22% drop during a recession is hardly a Great Depression collapse; its not even a Great Recession drop. Indeed, that line of thinking ignores the overhang of housing, the deleveraging consumer, and tight credit conditions — all of which could easily persist for years to come.

Bottom line: The Reagan Recession came at the end of a 16 year bear market, plus benefited from Volcker breaking the back of inflation. The threat today is a Japan like deflationary spiral, including falling asset prices and an unwillingness for investors to buy up for a dollar of earnings.

In other words, a falling P/E could be evidence of an ongoing deflationary phase, and not proof that markets are cheap.

The World’s Supreme Test for Gold

This excerpt comes from The Vancouver Sun of October 1933. It is a fascinating article. I strongly recommend that you read it in its entirety here. (It should take you no more than 3 minutes to do so.)

The article wrestled with one economically-perplexing question: Did gold become money because people wanted gold in a “special way” or is gold wanted by people just because gold is considered (legal) money? The article remarked that some economists believe it is the former, while others believe it is the latter.

The article---and its question posed---must be understood in context, however. In April of 1933, U.S. President Franklin D. Roosevelt ordered that all gold held by American citizens was property of the United States Treasury and, as such, by May 1933 all American citizens must turn in their gold to the Federal Reserve and/or an affiliate banks.

In other words, gold was no longer deemed (lawful) money in the United States. The article, therefore, pondered the question: Would the demand for gold remain even though the metal was no longer considered money?

The article’s author took the position that, regardless of if gold is deemed legal money, people want gold and that is what ultimately drives its demand. But gold was still considered money in other countries like France, Italy, Belgium, Germany, Holland, and Switzerland. In fact, the author noted that “Frenchmen” were regularly entering into the London Gold market to purchase gold even though it cost those business men a heavy premium compared to simply redemption at their own Bank of France. Why pay this premium?, the author asked. No need to ask why; just note that it is happening, the author said.

But what if the above-mentioned countries followed suit with the US and Britain and made gold “not money” anymore? What then for the demand for gold?

Time will tell, the author concluded.

Let us hope that if [the test of gold] materializes we shall profit by its lesson, for that lesson will be of great importance in clearing people’s minds upon some fundamental principles concerning the nature of “money”---and its “management.”

The author would be satisfied to know that history has answered this question and, in addition, has vindicated his position---that gold is desired and wanted by the people not because it is deemed legal money but because it is the truest money. After 70 years, history has proved that people desire gold regardless of what governments call it or deem it.

And right now---at a gold spot price at about $1900 per ounce---the people are showing their strong desire for gold is only beginning to be rekindled. The “supreme test” of gold has been completed. But it has not ended. Not until, that is, gold has been deemed “legal” money once again.

Gold is money.

Low Rates Are Goodand Bad

Borrowers breathed a collective sigh of relief when the Federal Reserve said earlier this month that it would hold interest rates at rock bottom for the next two years. But savers were far from happy.

"The news was a little depressing" for savers, says Jim Chessen, chief economist at the American Bankers Association. "It means low savings rates will be par for the course for the next couple of years."

A divided Federal Reserve conceded Aug. 9 that the economy was weak, with "downside risks" on the rise, and announced, surprisingly, that it would extend near-zero short-term interest rates another two years.

The Fed sets a "target rate" that banks follow closely when setting the "federal-funds rate" they charge each other for overnight loans as well as the competitive interest rates they charge consumers and businesses.

The Fed's move was aimed at goading consumers and businesses to look again at leverage as a means of investing in the economy -- either through big-ticket purchases like houses, cars and large appliances, or, for businesses, in equipment, new systems and even workers. The Fed's thinking is that if interest rates stay low enough, people and businesses won't be afraid to borrow, which could shake this stagnant economy back into growth mode.

But it stings if you're on a fixed income facing rising costs for energy and food, or if you're so wary of your money disappearing in the stock market that you're sitting on a bank savings account full of cash. Most bank-savings rates are below 1%.

Low interest rates hurt, too, if your retirement is dependent on interest income from certificates of deposit. Interest rates on a one-year CD have plunged to 0.42% from 2.38% just three years ago, according to Bankrate.com. Most money-market mutual-fund yields are at 0.01%. And at those rates, there's no wiggle room for inflation, which was 3.6% in the last year.

"It doesn't matter if your money is liquid or tied up in a CD, the yields right now do not compensate you for inflation," says Greg McBride, senior financial analyst at Bankrate.

Though the interest is adding only dimes and nickels to many savings accounts now and for the next two years, a federally insured bank is still a good bet to stash your cash.

If you're a homeowner with, say, a 5-1 adjustable-rate mortgage that's already past five years of the fixed-rate portion, you're in pretty good stead for the next couple of years.

Ditto on those home-equity lines of credit, which carry variable interest rates mostly based on the prime rate, which also trends with the federal-funds rate.

Low interest rates also have contributed to 50-year troughs in mortgage rates, which are determined by a variety of interest-rate benchmarks. Freddie Mac reported the average rate on a 30-year fixed-rate mortgage rose modestly last week to 4.22%, after seven straight weeks of declines. A year ago, the 30-year fixed-rate mortgage stood at 4.36%. The 5-1 ARM slipped to 3.07%, a record low.

Low interest rates are a positive for credit-card holders, unless, of course, you don't pay your bills on time and get slapped with high penalty rates. Thanks to the Credit Card Accountability, Responsibility and Disclosure Act, most banks reset their annual percentage rates to variable terms, meaning they could rise -- and fall -- along with the prime rate.

"It doesn't look like there's going to be any cost-of-funds pressure on credit-card issuers to increase" annual percentage rates, says Ben Woolsey, director of consumer research at CreditCard.com. The cost of funds refers to the rates banks charge each other on overnight loans. "It appears that banks are opening up more credit to people with excellent credit."

A low-interest environment makes it even more important that you pay off your credit-card balances, however. Because you're earning very little return on savings accounts and CDs, the amount you pay in interest-rate charges has more impact on your total budget and cash flow. Generally, interest earned on savings accounts can help offset the interest paid on credit cards.

The U.S. Dollar is a BUY (So The Calculations and Experts Say…)

By most “standard” calculations, the U.S. Dollar (USD) is undervalued by close to 20%. Using the Effective Exchange Rate methodology, the USD may be due for a rise in the near future.

However, even with the recent market slide and persistent worries over potential defaults within the EuroZone, traders have been avoiding the USD to a point where it is close to the lowest relative value that has been observed in decades.

Calculation methodology: An effective exchange rate is a measure of the value of a currency against a `basket’ of other currencies, relative to a base date. It is calculated as a weighted geometric average of the exchange rates, expressed in the form of an index. The effective exchange rate indices for sterling and other currencies published by the Bank are based on the method the IMF uses to calculate effective exchange rates for a number of industrialized countries.

The weights used are designed to measure, for an individual country, the relative importance of each of the other countries as a competitor to its manufacturing sector. The trade weights reflect aggregated trade flows in manufactured goods for the period 1989 to 1991 and cover 21 countries. The base date for the index is 1990, and is set at 100.

Now that additional QE appears to be off the table (or at least postponed for some time), gains on the USD may no longer be met with knee-jerk selling. If Bernanke and the team are discontinuing their support for a quick debasing of the currency, the safety net may have been pulled away.

There was an interesting story that appeared in Bloomberg that may provide an additional argument for the potential for the USD to rise:

The dollar is poised for its biggest monthly gain since May, reclaiming its status as a haven while Switzerland and Japan boost efforts to weaken their currencies. The U.S. currency has appreciated 1.2 percent in August against a basket of the developed world’s nine most-traded exchange rates, according to data compiled by Bloomberg. That compares with a decline of 14 percent in the world’s reserve currency from this time last year through July.

Demand for America’s assets is rising even though the Federal Reserve has pledged to keep its benchmark interest rate near zero through mid-2013 and Standard & Poor’s cut the nation’s credit rating from AAA. The two other currencies considered havens in times of financial and political strife — the Swiss franc and yen — are under siege by their governments and central banks after rising to records.

“The dollar is a buy through the end of the third quarter,” Nick Bennenbroek, head of currency strategy in New York at Wells Fargo & Co., the third-most accurate forecaster in the last six quarters as measured by Bloomberg, said in an Aug.

Currency forecast survey by Bloomberg:

Richard Poulden talks with James Turk

Richard Poulden, Director of Power Capital Financial Trading (PCFT), and James Turk, Director of the GoldMoney Foundation, talk about the new Pan Asia Gold Exchange (PAGE) and its potential to change the gold market with its allocated gold contracts.

They talk about PAGE’s plan to start trading in standardized 10 troy ounce gold bar contracts. Poulden expects local contracts to start trading in Q4 2011 and international contracts to follow in Q1 2012.