Talking about catastrophe is never fun, but avoiding the conversation can leave you unprepared and vulnerable. Worse it can lead to rash decision making if catastrophic events do occur. Preparing for a potential catastrophe is generally most successfully done when we are calm and clear headed. Furthermore, it is typically a good idea to purchase insurance during these placid periods in order to hedge ourselves against potential future storms. In this instance the future storms that loom over the US stock market and the US dollar--at least in the short term--are the end of QE2 this Summer, and the potential outcomes of the debt ceiling debate. The object of this article is not to discuss political ideology, but rather to discuss the potential negative outcomes from these two events, and a possible way to hedge a market collapse using VIX call options, or VIX ETNs like the iPath S&P 500 VIX Short-Term Futures ETN (VXX) and iPath S&P 500 VIX Mid-Term Futures ETN (VXZ).

The Volatility Index "VIX"

In a 2008 research paper written by VIX creator Robert E. Whaley, the author writes that "the VIX is a forward-looking index of the expected return volatility of the S&P 500 (SPY) index over the next 30 days. It is implied from the prices of S&P 500 index options, which are predominantly used by the market as a means of insuring the value of their stock portfolio." Thus the VIX essentially analyzes the difference between call and put options on the S&P 500 that expire in the next 30 days. For a thorough discussion of the VIX pricing methodology please see the Chicago Board of Options Exchange "CBOE" VIX white paper (pdf).

Simply put, a call option is a contract between two parties where the purchaser believes the underlying investment will go up in time, and the writer of the contract typically believes the price of the underlying asset will go down or stay even. The contract premium is what the call writer collects from the call buyer, and this premium varies depending on a number of different factors. In general a call buyer will make money if the price of the underlying asset goes above the agreed upon strike price during the period of the options call contract. Conversely a buyer of a put contract is making a bet that a stock or the underlying asset will go down over time, and the put writer is collecting a premium for the bet. Also the put writer is typically betting that the stock won't go down; however it should be noted that there are certainly exceptions to these generalization.

These call and put contracts get much more complicated than my simple explanation, but it's important to understand the relationship between the put and call option contracts as they relate to the VIX. For instance, in a bull market the VIX will typically be very low, as there are more bets that stocks will increase in value over time, and in a bear market the exact opposite is true. Below is a chart put together by Dr. Whaley that looks at the relationship of the VIX to the S&P 500 from 1986 to 2008. The Blue line represents the S&P 500, and the red line represents the VIX.

It should also be noted that the VIX is intimately tied to liquidity. In a robust market with many participants liquidity is high as it is easy to find buyers and sellers. However, in times of panic a market becomes temporarily illiquid as the number of sellers far outweigh the number of buyers. This dislocation between buyers and sellers causes large spreads to occur between a seller's ask price, and a buyer's bid. The result is a large drop in value as desperate sellers capitulate and sell to the few buyers left in the market. This short period of illiquidity results in a spike in the price of put options as traders look to short stocks, and a spike in the opposite direction for call options as traders fear taking on bullish risk. The end result is a turbocharged VIX that can make a large percentage move in a day.

In the past 15 years several instances of large VIX jumps have occurred. The Asian Currency Crisis of 1997 and 1998, the Russian Default Crisis of 1999, the September 11th terrorist attacks, and the Lehman Default of 2008 are all prime examples of large percentage jumps in the VIX. As you can see the VIX is highly susceptible to black swan events and sovereign defaults. The chart below was created by Artemis Capital LLC to look at the impact of sovereign currency crises on the VIX. The orange area looks at the Mexican Peso crisis, the Yellow Area reviews the Asian currency crisis, and the red area is the Russian Ruble default.

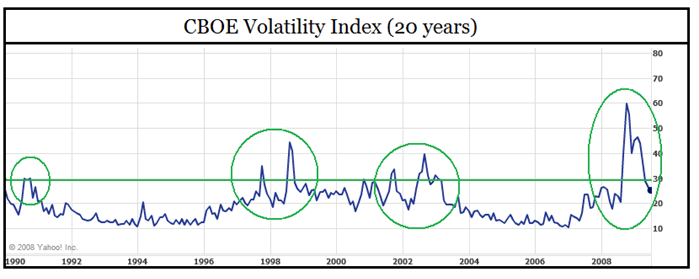

(Click charts to enlarge)

The chart below is a 20 year history of the VIX. The first green circle corresponds to the Mexican Peso Crisis, the second circle is the Asian and Russian crises, the third circle indicates the September 11th attacks and the 2002-2003 recession that followed. The last circle indicates the 2007 housing crisis and Lehman Bankruptcy. As you can see in periods of market distress, particularly during sovereign credit crises, the VIX has a very large and punctuated percentage gain.

Why the VIX is a Good Investment Now

According to Dr. Whaley's 2008 paper, the 22 year average value for the VIX is 18.88. Typically as a rule of thumb a VIX reading below 10 indicates a very placid market with little fear and good fundamentals. A rating above 20 indicates a tepid market with some risk, a rating above 30 is generally indicative of concern over fundamentals, and a rating above 40 illustrates panic in the market place. As of Friday's market close on 4/22/2011, the VIX stood at 14.69.

The low VIX reading for the market is due to several factors, but mainly is a function of Quantitative Easing conducted by the Federal Reserve. As mentioned earlier, the VIX generally has an inverse relationship with liquidity. If liquidity remains high then the VIX will generally go down. However, when liquidity is threatened, the VIX as well as the stock market will typically spasm simultaneously in opposite directions. Knowing this the Federal Reserve has attempted to induce risk investments in equities by keeping interest rates low, and by purchasing asset classes that other investors may not want like mortgage backed securities "MBS" and U.S Bonds.

The impact of the Federal Reserve's efforts has allowed institutional investors to borrow money at low rates, and seek higher yields in other asset classes like commodities, equities, and options. These efforts have in large part helped spur the current bull market in equities and commodities. However, once the Federal Reserve stops it's QE2 program, liquidity in the markets will start to dry up as there will be fewer buyers propping up the bond market. The impact of this will potentially force an interest rate rise as sovereign nations and institutional investors demand a higher return on their investment in US bonds.

In addition to the problems raised by the end of QE2, the US needs to make a decision on whether or not to raise the country's debt ceiling. If the US. does decide to raise the debt ceiling the likely short term results could be a weaker US dollar, an increase in commodity prices, and a potential interest rate hike. If the US decides to delay or vote down the proposal to raise the debt ceiling the result would most likely be very bearish. Possible consequences of a failure to raise the debt ceiling include: a wave of government sector firings, sovereign nations like China and Japan dumping large amounts of US. debt, a large interest rate spike as sovereign nations would value our debt at a much lower credit rating, a short spike in commodity prices particularly gold, and a slow down in the American economy as businesses may have difficulty finding credit. Furthermore, the likely result of a delay or a refusal to raise the debt ceiling would be a quick and immediate spike in the VIX as traders become bearish on the US. equity market.

The VIX As Life Insurance for Your Portfolio

The confluence of the above factors makes the VIX an attractive purchase at these levels. The factors previously discussed are: the low VIX price relative to it's historical average, the end of QE2, and possible market turbulence as the result of the debate over the US debt ceiling. For those with substantial equity positions, it may be a good idea to consider the VIX as an insurance product that can protect your portfolio against potential financial disasters. Furthermore, the price of the VIX insurance premium is quite low relative to it's historical average, and the chance for near term market turbulence is in the author's opinion quite high.

As an analogy, view your portfolio as if it was a young 35 year old with no real health complications. The price of purchasing life insurance for your portfolio in this instance would be quite low because there are few perceived risks at the moment. However, if the market goes down and liquidity dry's up, then your portfolio may look more like a 70 year old chain-smoker. The cost of insuring this portfolio would be quite high relative to the other portfolio. While you may risk losing your insurance premium if the market remains bullish, at least you'll be getting a historically low premium rate.

How to Play the VIX

Institutional investors, and investors with large portfolios can purchase call option contracts from the Chicago Board of Options Exchange (CBOE) with varying maturity dates. The contracts are European style meaning that the option can only be exercised at the maturity date. Investors who prefer not to trade options can invest in Barclay's short term VIX ETN (VXX) or medium term VIX ETN (VXZ). Whether an investor decides to invest in CBOE VIX call options or ETNs it's recommended that the investor only take a small position in these securities since they are simply insurance against your portfolio losing value.

If investors do purchase the VXX or VXZ, it may be a good idea to consider placing a limit order at a reasonable return as the VIX can sometimes spike quite quickly, and only a nimble trader would be able to sell out at a large profit. Furthermore, investors are encouraged to consider the risks of purchasing VIX call options, or the Barclay's VXX and VXZ ETNs. Particular attention should be given to the fact that the VXX and VXZ methodology often create a contango situation that can lose an investor a considerable amount of money over time. For this reason, it is recommended that investors who choose to invest in the VXX or VXZ have a short term perspective of 3 months or less so that only a small amount of principle will be lost if the stock and bond markets remain bullish.

Conclusion

In summary, investors should consider buying insurance for their stock portfolio through either VIX call options, or a VIX ETN. As discussed in the article the VIX may provide a hedge to an investor's portfolio against potential near term financial headwinds. The US debt limit debate, and the end of QE2 present two such headwinds that may create turbulence in the markets. Additionally, the low cost of purchasing a VIX insurance premium means that this investment has relatively little downside risk. As always investors are encouraged to do their own due diligence, and to consider their risk tolerance before taking a position in the VIX.

No comments:

Post a Comment