I did some research on the VIX about fifteen years ago that I subsequently filed away for a later date. This may be good time to bring it forward and get some discussion on it.

The research presents a very simple and quick way to determine when options players are acting “rationally” or “irrationally” about the market; that is, if the VIX implied market volatility actually matches real market volatility (rational), or if the VIX is over- or under-stating it (irrational). It’s based on the idea that the VIX doesn’t really tell you anything by itself. It’s only when you compare it with the market’s actual volatility that it really does say something unique.

What is the VIX?

One major problem with the VIX is that few investors know what it really is. In fact it’s even been given a wrong name. It’s called the fear index although it’s anything but. The entire subject of the VIX and even options themselves starts with something called the Black Scholes equation for options pricing; a thing considered so important it actually won the economist Myron Scholes a Nobel Prize in 1997.

In this equation you insert the option’s strike price, the current stock price, as well as the time remaining before option expires. You also insert a riskless interest rate but don’t ask why; it’s not as critical as these other factors by a wide margin. Lastly, you insert the stock’s volatility number. Like magic, the equation spits out the theoretical price you should pay for that option. What anyone did before this equation is anyone’s guess.

The Volatility Calculation

Of all these inputs the only confusing one is probably the volatility number. How is a stock’s volatility calculated? Essentially you go back five or ten years and do these day-to-day calculations on price and from these you get a number that represents the yearly price variation of that stock. This procedure works fine if the option in question is long term, say six to nine months from expiration. There, any sudden short term change in volatility from a news item dampens out over time. When pricing a long term option you use this stable number; you don’t use any short term volatility number; it won't work well.

However, when pricing a shorter-term option, say one expiring in a month, this long term number doesn’t work well. You must use a shorter term calculation of volatility. You might use a ten or fifteen day volatility calculation. While this calculation will vary widely it will more accurately reflect the market conditions that will apply to that option over its shorter lifetime.

The VIX is 'Implied' Volatility

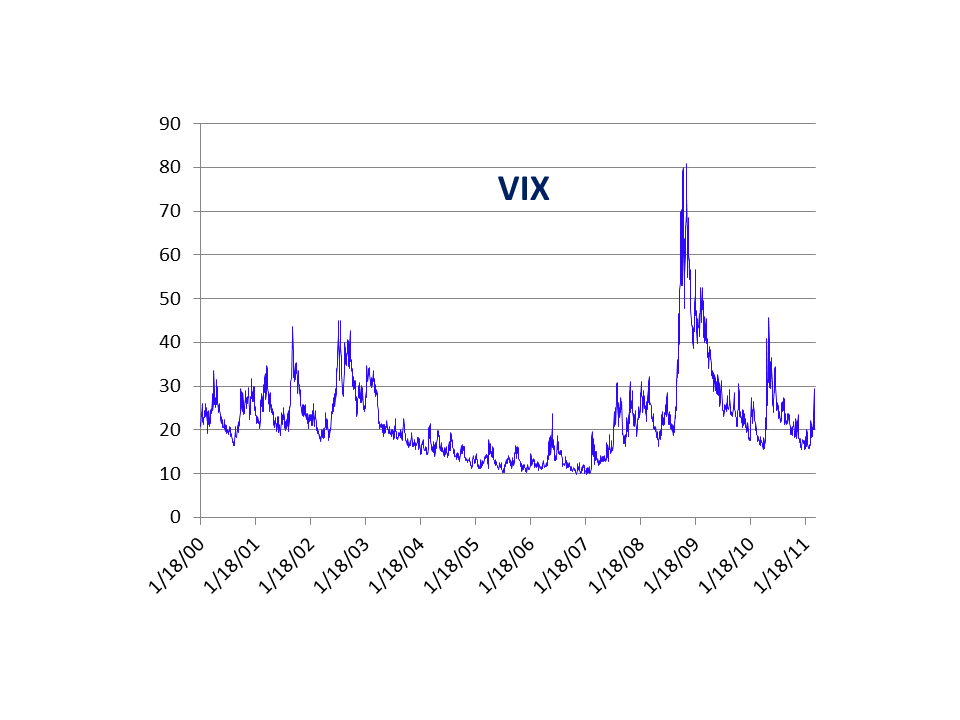

Now here is where some market technician got ingenious. Someone thought, “Instead of doing this short-term calculation all the time, let’s calculate backwards. From the latest option price let’s figure out the volatility number traders are assuming at that moment.” This backward calculation is the VIX and it's why it’s called “implied” volatility; it’s the volatility number that’s “implied” by the Black Scholes equation using the most recent short-term option prices of the S&P 500 (SPY). The VIX for the last eleven years is shown in this first well-known chart below.

Implied Volatility vs. Real Volatility (almost)

Much has been written and spoken about the VIX, but in my opinion the VIX doesn’t indicate or say anything in itself. Maybe the VIX is simply measuring the real changing short-term volatility of the market and not telling us anything we don’t already know. To see if it is, we could calculate the market’s actual short-term volatility and compare it with the VIX’s implied volatility. However, in doing this I’ve personally found it more useful to do another calculation of volatility over the standard formula. It's also simpler to do. It’s based on the fact that traders are much more alarmed by large day-to-day fluctuations in the market than the actual volatility number that theory might produce.

A Simple Modified Volatility Number

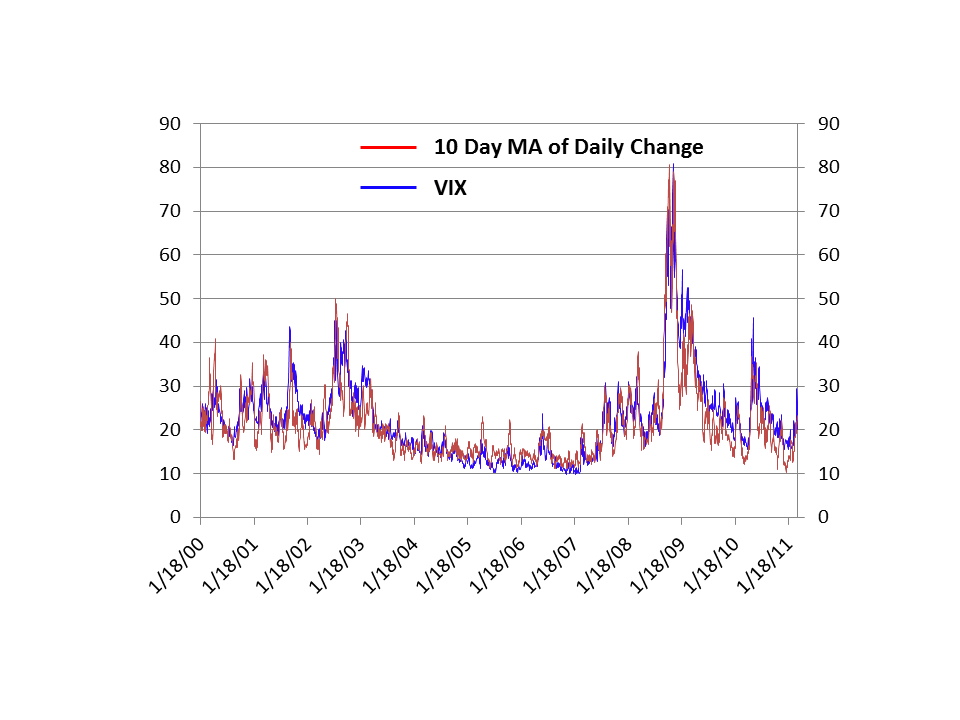

If the market goes up and down 3% a day, but over time doesn’t go anywhere, that will show as a low volatility calculation. Yet we know that investors will not (rightfully) consider it so. Just like a person jumping and going up and down ten feet in the air, they may not get anywhere but they will still cause a lot of commotion. Because of this a more accurate idea, in my opinion, is to simply calculate the average absolute value of the daily percentage change in the market over a short time period. The second chart shows this; it plots the VIX index (blue) against a simple 10-day moving average of the absolute daily price change in the S&P 500 (red). The two numbers are normalized (put on the same scale) by using a simple conversion factor that does this.

The Details

Experience with market psychology or investor sentiment over many years shows what is usually important when expectations get either too one-sided or when they don’t match what is really happening. For example, if the market rallies and investor are doubtful that is usually a good sign; the market is rising against a wall of worry. In a similar vein with the VIX, what should be important is not when the VIX matches real market volatility but when the VIX diverges from what is really happening volatility-wise. It’s when the market calms down, yet investors remain doubtful and jumpy. Or when real volatility rises, but options players ignore it and remain complacent.

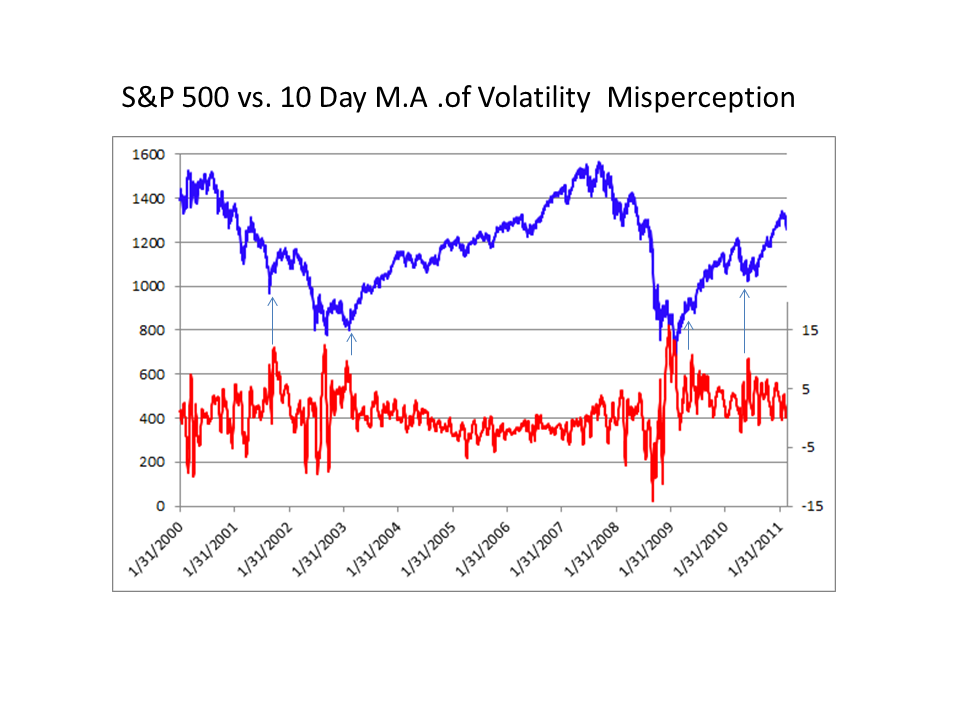

Because of this what should be important is not the similarity in the two numbers but when they become widely different. The third chart shows this difference - the difference between the VIX and a smoothed version of the 10-day moving average of the daily absolute changes in the market. High numbers are when the VIX is overstating volatility (probably a bullish indicator) and low numbers the opposite.

There is one point this comparison made very clear last week. The recent surge in the VIX last week in response to the market decline and the Japanese catastrophe was a rational investor response. The increase in the VIX implied volatility pretty much matched the actual increase in market volatility.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

No comments:

Post a Comment